Could Co-Buying Be the Answer for Some First-Time Buyers?

For a lot of would-be first-time buyers, affordability is the thing that’s standing in the way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying.

The Dream Is Still Alive. The Math Just Isn’t Working for Everyone.

Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation.

The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases, the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981.

But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door.

So, What’s Co-Buying?

Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner.

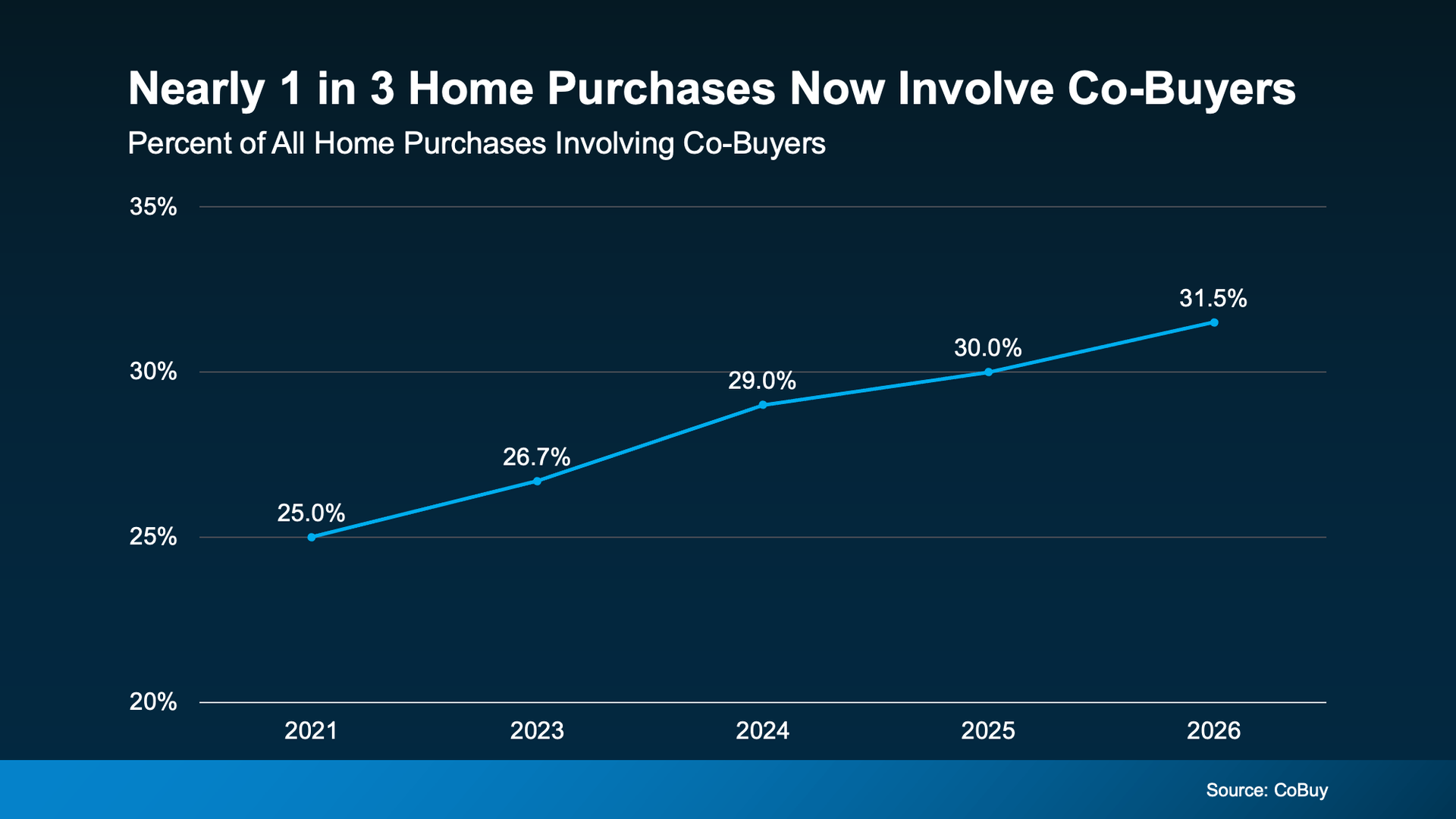

And it's catching on fast, just look at where things stand today. According to CoBuy.io, 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below):

Why It Works

Here are just a few of the top reasons buyers are going this route, according to NerdWallet:

- Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours.

- More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own.

- Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers.

- Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting. Plus, sharing costs can make repairs or renovations more manageable, too.

Things To Keep in Mind

If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road.

That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment.

Bottom Line

Affordability challenges are real, but they don't have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots all over California, including Roseville, Folsom, Sacramento and everything in between!

If you're curious whether it could work for your situation, let's talk. Reach out today and let's figure out your path to homeownership together.