What Rising Inflation Means for Your Move

Data shows inflation is moving in the wrong direction. But before the headlines send anyone into a panic, here's what's actually going on, why it matters for the housing market, and what it means if you're thinking about buying or selling.

Inflation Went Up – Here’s What That Actually Means

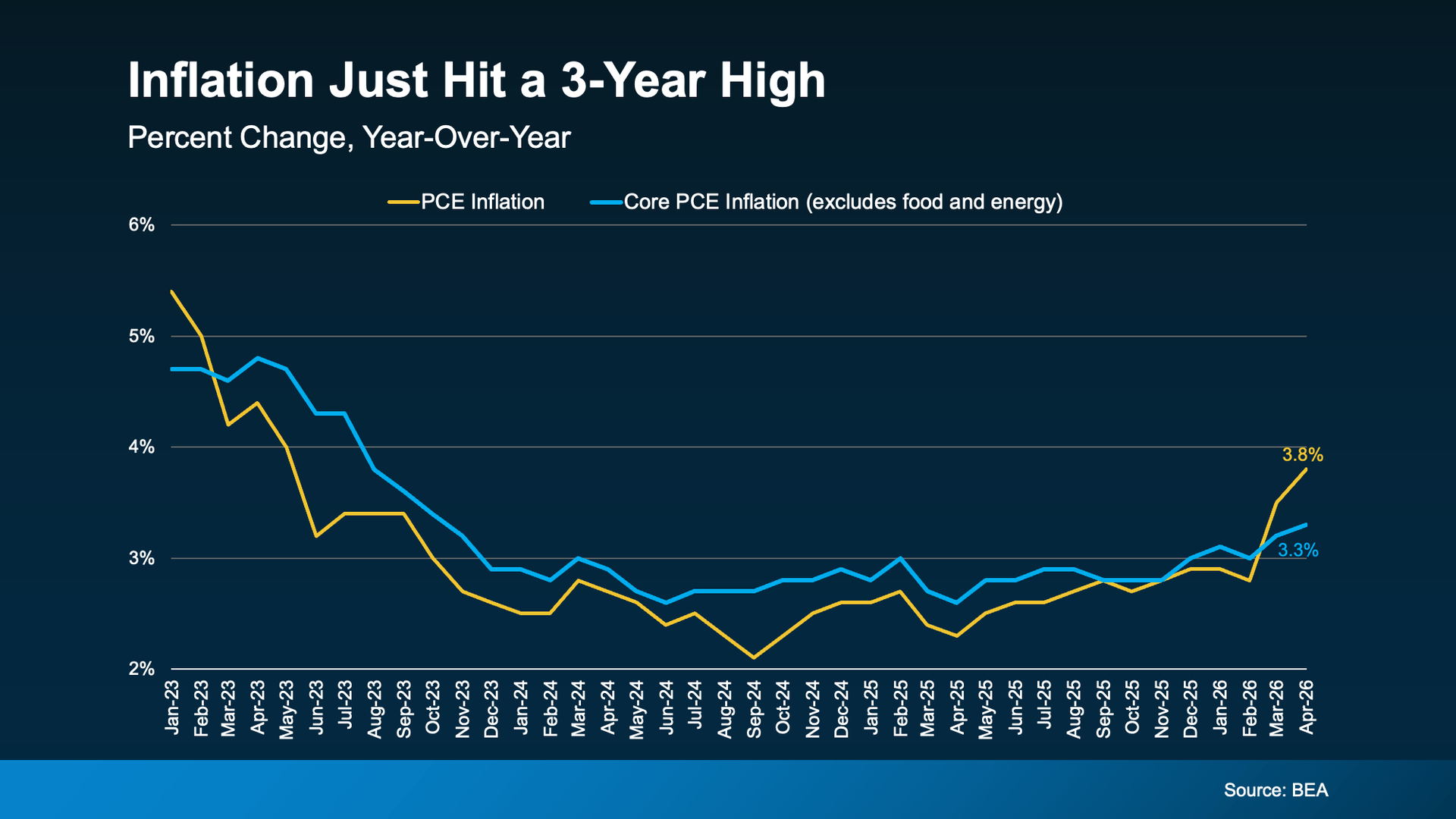

The government tracks inflation in a variety of ways. One is something called PCE – the Personal Consumption Expenditures Price Index. It measures how much more (or less) people are paying for goods and services compared to a year ago. And just based on your own expenses, you can probably guess which way that’s trending.

That’s the one everyone is talking about right now. Check out the yellow line to see how that’s spiked since February (see graph below). A big driver of this jump is the ongoing conflict in the Middle East, which has pushed gas and energy prices significantly higher.

Now, you may have noticed there’s a second line. The blue line shows core PCE. That’s the same measure, but with gas and energy prices stripped out. The Federal Reserve (the Fed) actually watches this number most closely because energy prices swing around a lot and can be misleading.

And here’s the somewhat encouraging part.

Core PCE is rising, but not nearly as fast as the overall number. That suggests a good chunk of the inflation spike we’re seeing right now is tied directly to what’s happening overseas. So, when that situation settles down, inflation may settle a bit, too.

Why This Matters for Mortgage Rates

Here's the housing connection. When inflation is high, the Fed tends to keep the Federal Funds Rate elevated or even raise it to try to taper spending and cool inflation back down. And while it's not a one-for-one relationship, that Federal Funds Rate can have an impact on your mortgage rate when you buy.

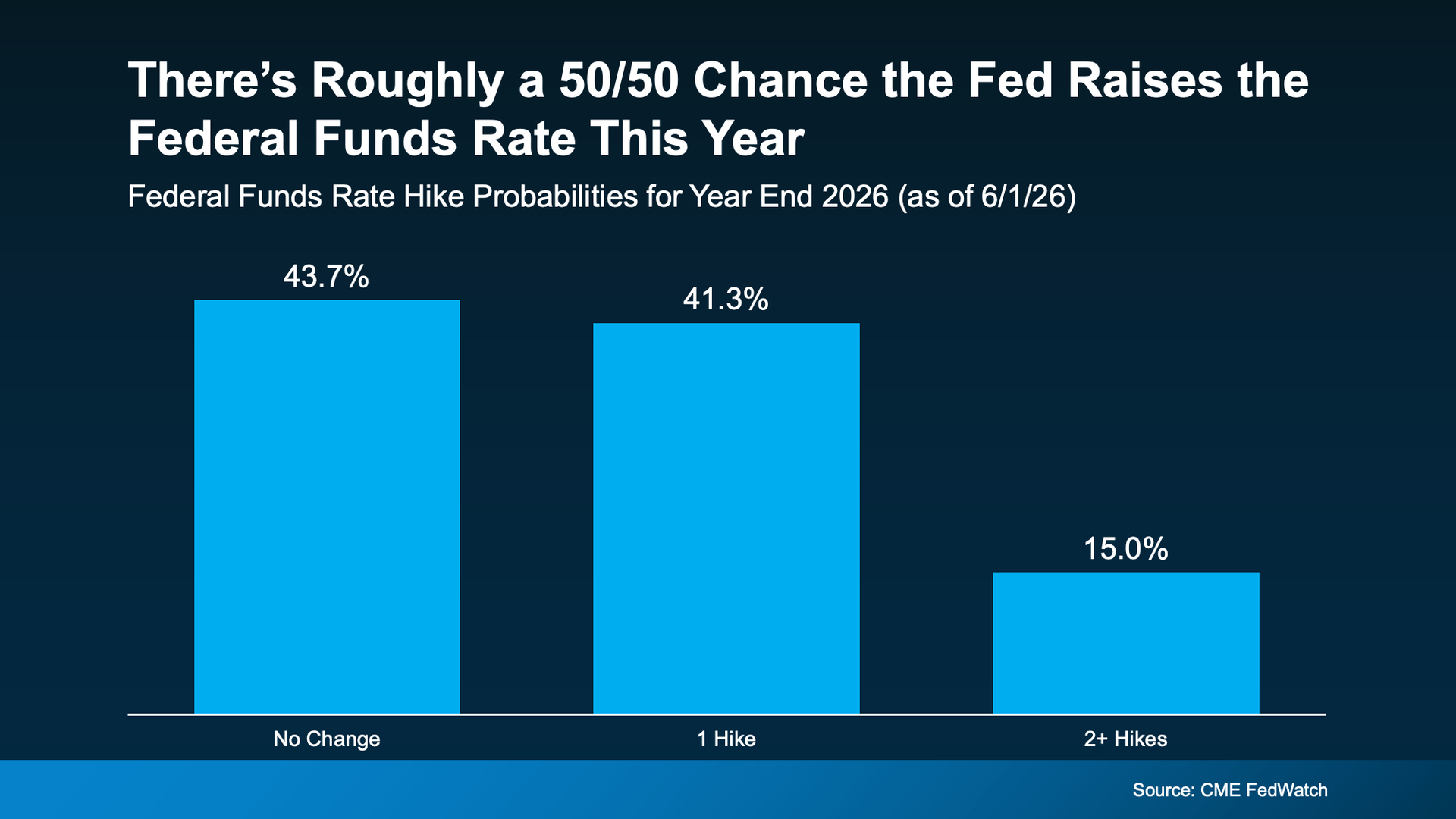

Right now, based on the information we have, there's roughly a 50/50 chance the Fed actually raises the Federal Funds Rate before the end of 2026, according to CME FedWatch (see graph below):

While it’s too soon to say where this goes for certain and if we’re headed for a rate hike, it does mean mortgage rates are probably not coming down as soon as most people were hoping.

If you've been waiting for rates to drop significantly before making a move, this report is a reminder that "higher for longer" is still very much on the table. It really all depends on where the economy goes from here. According to Bankrate:

“Oil prices and bond yields have dropped a bit . . . but they're still way up compared to the start of spring. Until there’s a resolution to the war, look for both inflation and mortgage rates to stay high.”

But This Is Not 2008 – Not Even Close

Just remember, a tough economy does not equal a housing crash. The conditions today are very different from what led to the 2008 collapse. Here's why:

- Inventory is still relatively low. There's no flood of homes hitting the market.

- Most homeowners today have strong equity in their homes.

- Lending standards are far stricter than they were before 2008.

- Today's challenge is affordability, not a wave of distressed underwater sellers.

Uncomfortable and unhealthy are not the same thing. The market feels hard right now, but "hard" and "crashing" are very different.

You Still Have Options. Here’s What To Do.

High rates does not mean homeownership is out of reach for everybody. It just means the path looks a little different for many. There are real strategies that can help, depending on your situation:

- Ask your lender about different loan options. Adjustable-rate mortgages (ARMs) or rate buydowns may help lower your monthly payment in the short term.

- Explore first-time buyer programs, down payment assistance, or seller concessions that could help offset costs.

- Stay in close touch with a trusted agent and lender. When rates shift, and they will, you’ll want to be ready to move fast.

The right strategy, tailored to your goals, matters a lot more than waiting for the perfect moment that may never come.

Bottom Line

Inflation is still above where the Fed wants it, and that means mortgage rates are likely to stay elevated for a while. But for people who need to move, strategy matters far more than trying to perfectly time the market.

Wondering what this means for your specific situation with buying a new home in Roseville, Rocklin, Granite Bay, or anywhere in the Sacramento Valley? Let's cut through the noise together and make a plan that actually works to help you and your family into home ownership. After all, your paying a mortgage even when you are renting, its just you are paying someone else's mortgage, building their equity, and losing out on your own equity growth and your own tax advantages of being an owner. Reach out to me today and we can put together a plan to help.