Homebuilders Aren’t Overbuilding, They’re Catching Up

Did you know that I also sell new houses, not just resale houses? I do, and quite often it's because my clients can not find a resale home that is in the condition and budget that my client wants to purchase. Many people have heard that there are more brand-new homes available right now than the normal resale homes, that is not true however about one in three homes on the market are newly built. And if you’re wondering what that means for the housing market and for your own move, here’s what you need to know.

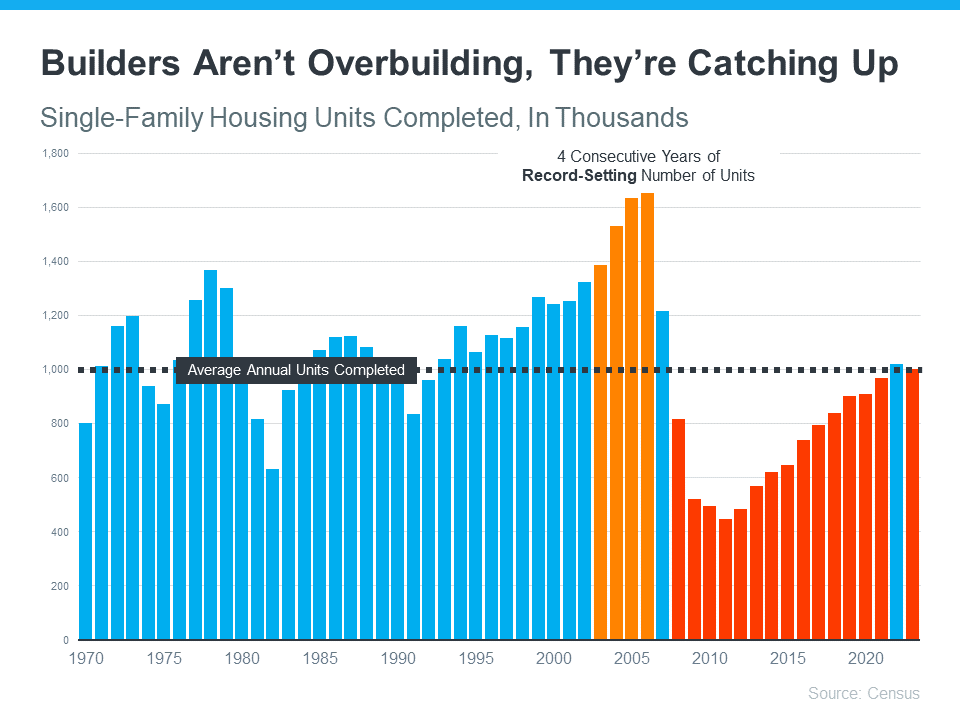

Why This Isn’t Like 2008

People remember what happened to the housing market back in 2008. And one of the factors that contributed to that crash was that there were too many homes for sale. While only part of the oversupply back then came from builders, the lasting impact is that some people still feel uneasy when they hear new home construction has ramped up.

Even though the supply of new homes has grown this year, the data shows there’s no need to worry. Builders aren’t overbuilding, they’re just catching up.

The graph below uses data from the Census to show the number of new houses built over the last 52 years. Following the crash in 2008, there was a long period of underbuilding (shown in red). And it wasn’t until recently that we finally met the long-term average for how many homes are built in a typical year.

This shows, that even with the increase in new builds we’ve seen lately, there won’t suddenly be an oversupply of homes for sale. There’s too much of a gap to make up after over a decade of underbuilding. And if you’re still worried builders are overdoing it, here’s something else that should be reassuring.

New Home Construction May Be at Its Peak for the Year

The latest data from the Census on housing starts (homes where builders just broke ground) and permits (homes where builders can start development soon) shows builders are slowing down their pace right now. Why is that?

They’re responding to still high mortgage rates and how those are impacting buyer demand. Basically, they’re pulling back appropriately in response to what’s happening in the market. As an article from HousingWire explains:

“Even with a massive housing shortage across the nation, homebuilders are completing their pipelines and not seeking as many permits to construct new single-family houses.”

Builders remember what happened when they overbuilt in the crash, and they’re looking to avoid a repeat of that. So, they’re being mindful and pulling back a bit.

You May Have More Options Now Versus Later

If you’re considering a newly built home, here’s how this impacts you. With builders seeking fewer permits and not breaking ground on as many new homes, we may be at the peak of new home construction for the year. This doesn’t mean new home construction is screeching to a stop – just that the pace is slowing down now, and that’ll impact what comes to market later this year. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Given the recent declines in housing starts, home completions will steadily show declines in about six months.”

So, if you’re ready and able to buy now, you may find you’ll have more newly built options to choose from now versus later on. This may be enough reason to kick off your search.

Just be sure to work with a local real estate agent like me that you know and trust throughout the process. I have valuable experience and insight into builder reputations and other key factors specific to our real estate market in Roseville, Rocklin, Granite Bay. Lincoln, Folsom, El Dorado Hills, and of course Sacramento.

Bottom Line

While it’s true new home construction is a bigger segment of the market than the norm, that’s not a bad thing. Builders aren’t overbuilding, and they’re responding to market signals to avoid repeating the mistakes that were made in 2008.

If you want to buy now while new home options may be at their peak, let’s connect.