3 Key Factors Affecting Home Affordability

Over the past year, a lot of people have been talking about housing affordability here in Placer and Sacramento Counties, and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front. Mortgage rates have gone down since their most recent peak in October. But there’s more to being able to afford a home than just mortgage rates.

To really understand home affordability, you need to look at the combination of three important factors: mortgage rates, home prices, and wages. Let’s dive into the latest data on each one to see why affordability is improving.

1. Mortgage Rates

Mortgage rates have come down in recent months. And looking forward, most experts expect them to decline further over the course of the year. Jiayi Xu, an economist at Realtor.com, explains:

“While there could be some fluctuations in the path forward … the general expectation is that mortgage rates will continue to trend downward , as long as the economy continues to see progress on inflation.”

And even a small change in mortgage rates can have a big impact on your purchasing power, making it easier for you to afford the home you want by reducing your monthly mortgage payment. As a buyer you need to consider what you feel is affordable, while also thinking about the long term plan. A $400 difference in a payment to some buyers is huge, and to others it's not a big deal at all. You also must consider your position to buy.

A key factor to consider is that if your living at home, you are truly saving money but if your renting you are not. Unless you are living at home, or pay cash for your home, you are always making a mortgage payment. The key factor to consider is do you want to pay off someone else's debt or your own? If you are buying for your self than you get the equity gain in the future and the property will eventually be paid off and owned by you. If you are renting, then your landlord will get the equity gain in the future. Wouldn't you rather be paying off your own home, and getting your own equity gain?

2. Home Prices

The second important factor is home prices. After going up at a relatively normal pace last year, they’re expected to continue rising moderately in 2024. That’s because even with inventory projected to grow slightly this year, there still aren’t enough homes for sale for all the people who want to buy them. According to Lisa Sturtevant, Chief Economist at Bright MLS:

“More inventory will be generally offset by more buyers in the market. As a result, it is expected that, overall, the median home price in the U.S. will grow modestly . . .”

With the interest rates at a more normal rate, it has slowed down the housing market. Many people are staying inter homes longer as they are in love with the ultra low interest rates they got in 2020, and 2021 which means that there are less homes to buy. And less inventory to sell. This is keeping the prices stable. They are not likely to skyrocket like they did during the pandemic, however with the ultra low inventory to choose from the prices are not expected to go down either. However, it also means it’ll probably cost you more to wait for the rates to come down before you buy. So, if you’re ready, willing, and able to buy, and you can find the right home, purchasing before more buyers enter the market and prices rise further might be in your best interest.

The saying that I often hear is, date the rate, but marry your house. This is because you can always get a new interest rate by refinancing in the future if and when the rates come down, but you lock in the price of your house when you buy it. It always feels good to buy and know that no-one will give you a rent increase.

3. Wages

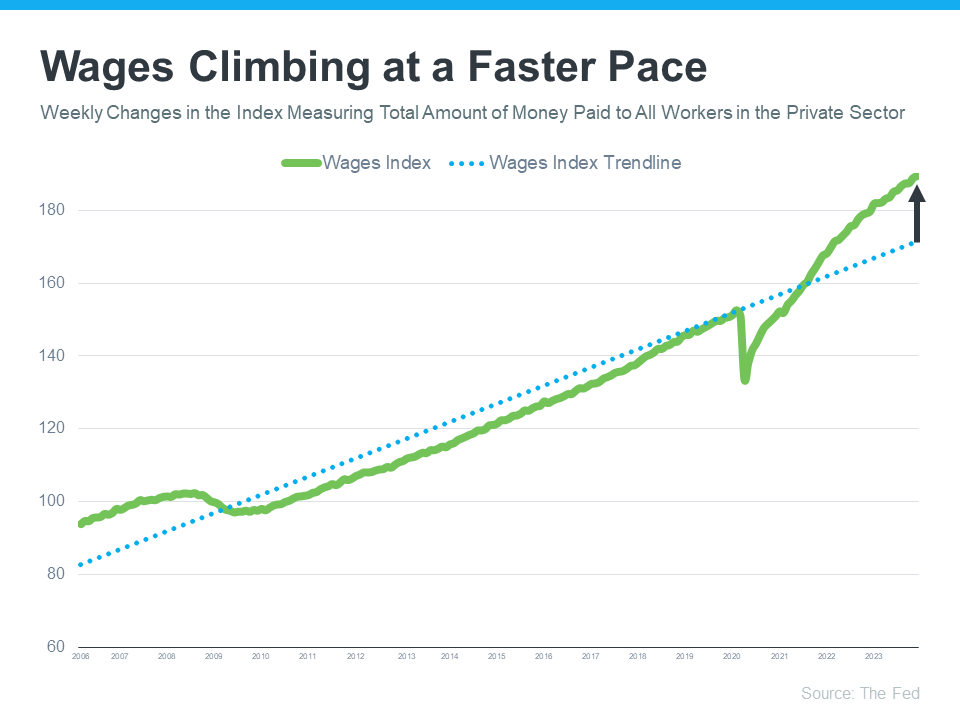

Another positive factor in affordability right now is rising income. The graph below uses data from the Federal Reserve to show how wages have grown over time:

If you look at the blue dotted trendline, you can see the rate at which wages typically rise. But on the right side of the graph, wages are above the trend line today, meaning they’re going up at a higher rate than normal.

Higher wages improve affordability because they reduce the percentage of your income it takes to pay your mortgage. That’s because you don’t have to put as much of your paycheck toward your monthly housing cost.

What This Means for You

Home affordability depends on three things: mortgage rates, home prices, and wages. The good news is, they’re moving in a positive direction for buyers overall.

Bottom Line

If you're thinking about buying a home, it's important to know the main factors impacting affordability are improving. To get the latest updates on each, connect with me, your top agent, your real estate professional who has grown up in Roseville, and Placer County. A professional who moved back to raid my family as I know the quality of life here is great! There is no place else like the Sacramento Valley. Whether you want to live in Granite Bay, Eldorado Hills, Roseville, Rocklin, Sacramento, or anywhere around our amazing community let's connect. Let's discuss what the home-buying process looks like for you and your family.